Accountancy: Deferred Taxes

DTL + DTA

BOOK TAX ≠ INCOME TAX

Caused by TEMPORARY DIFFERENCES

Deferred taxes refer to tax amounts that a company either owes or can recover in the future, resulting from temporary differences between its financial accounting and tax accounting. These differences arise because certain items are recognized at different times for financial reporting purposes (under GAAP or IFRS) and for tax purposes.

Types DT:

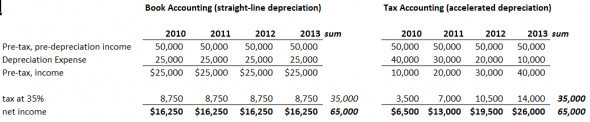

Deferred Tax Liability (DTL): This occurs when a company has to pay more taxes in the future. It happens when the company’s taxable income is lower than its accounting income due to temporary differences. For example, using accelerated depreciation for tax purposes but straight-line depreciation for financial reporting creates a DTL. The company defers part of its tax payment to the future, knowing it will eventually have to pay more.

This is the ideal result for a company. Reported income is maximised up front, but tax income is minimised, so cash taxes paid are lower. But over time, income and tax are equal.

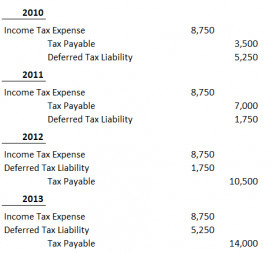

And this is what the accounting entries would look like over the years.

A common example that causes a DTL is the use of accelerated depreciation for tax purposes and straight-line depreciation for financial reporting

Deferred Tax Asset (DTA): This occurs when a company is expected to save on taxes in the future. It happens when the company’s taxable income is higher than its accounting income due to temporary differences. For example, if a company recognizes warranty expenses on its financial statements now but can’t deduct them for tax purposes until later, it creates a DTA. This means the company effectively "prepaid" its taxes and will benefit from lower taxes in the future.

A common example that causes a DTA may be caused when a company recognizes warranty expense for financial reporting but is not allowed to deduct this expense when preparing its tax filings.